Transfer Pricing (TP) refers to the pricing arrangements applied to goods, services, loans, and intangible assets exchanged between two or more enterprises that are part of the same corporate group or are otherwise related. This typically occurs within a multinational enterprise (MNE) group.

Point to Note: Transfer pricing (TP) is not an additional form of taxation; rather, it is a critical aspect of tax planning that directly influences liabilities such as Income Tax, Capital Gains Tax, and Value Added Tax. Inaccurate pricing of transactions between related parties can lead to substantial tax exposures. Effectively understanding and managing TP is essential for meeting tax obligations and maintaining compliance.

What is a Transfer Pricing Regime?

A Transfer Pricing Regime refers to the legal and regulatory framework a country or a group of countries adopts to govern how multinational enterprises (MNE) price transactions between their associated enterprises across borders.

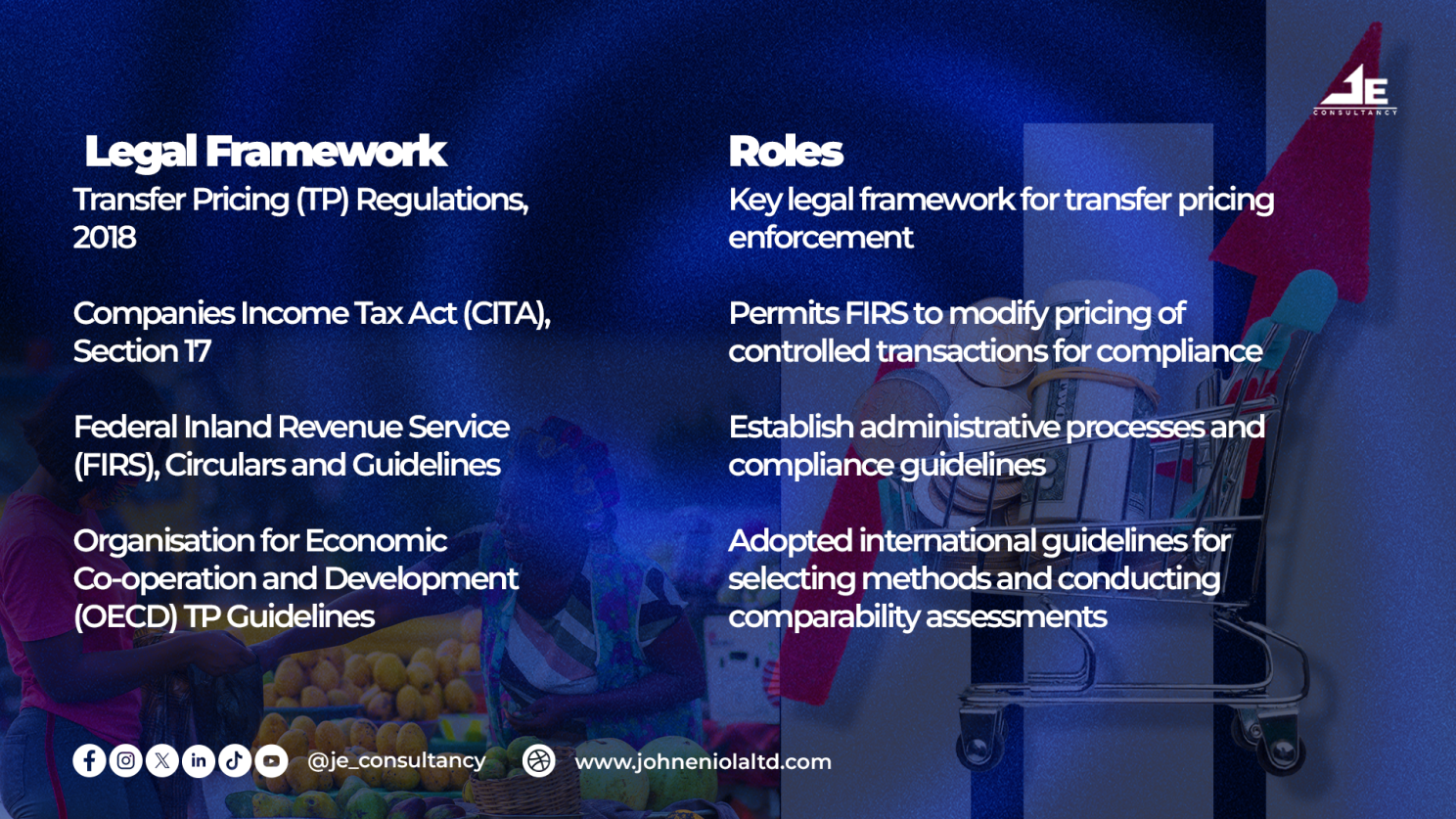

Laws Governing the Transfer Pricing Regime in Nigeria

Transfer Pricing (TP) Regulations were first introduced on 2nd August 2012 but were later replaced by the updated Income Tax (Transfer Pricing) Regulations 2018, which took effect on 12th March 2018.

Transfer Pricing (TP) Methods in Nigeria

The Nigerian TP Regulations recognise the following five primary methods for determining the arm’s length price:

1. Comparable Uncontrolled Price (CUP) Method: It is used to determine the arm’s length price for goods, services, or intangible assets exchanged between related entities, such as a parent company and its subsidiary.

2. Resale Price Method (RPM): This method is used to determine the arm’s length price for goods or services exchanged between related parties and is particularly effective when the product is resold to an independent buyer with little or no modification.

3. Transactional Net Margin Method (TNMM): This determines if related-party transactions are at arm’s length by comparing net profit margins from controlled transactions to those in comparable independent transactions.

4. Cost Plus Method (CPM): This is a transfer pricing method used to determine the arm’s length price in related-party transactions, particularly effective for goods or services involving manufacturing, assembly, or contract-based activities.

5. Transactional Profit Split Method: This is a transfer pricing approach used to fairly allocate profits between related parties when their activities are closely integrated and cannot be assessed independently.

Key Requirements for Filing Transfer Pricing Documentation

1. Transfer Pricing Declaration: The Transfer Pricing Declaration must be submitted to the Federal Inland Revenue Service (FIRS) within 18 months from the date of incorporation, or within six months after the end of the relevant accounting year, whichever occurs first. Additionally, any updates or changes to the initial declaration must be submitted to the FIRS within six months following the end of the accounting year in which the change occurred.

2. Transfer Pricing Disclosure: A transfer pricing disclosure of transactions must be submitted by a connected person to the Federal Inland Revenue Service (FIRS) voluntarily and without prior notice or demand, no later than six months after the end of each accounting year or 18 months from the date of incorporation, whichever comes first.

3. Transfer Pricing Documentation: A connected person is required to maintain, in writing or in any electronic format, adequate information and data, along with a supporting analysis, to demonstrate that the pricing of controlled transactions complies with the arm’s length principle. This documentation must be made available to the Federal Inland Revenue Service (FIRS) upon receipt of a written request.

4. Country-by-Country Report (CbCR): The Country-by-Country Report is required to be filed within 12 months following the end of the multinational enterprise (MNE) group’s reporting accounting year.

Benefits of Transfer Pricing

- Safeguards the National Tax Base: Restricts profit shifting by multinational companies to low or no-tax jurisdictions.

2. Ensures Fair Tax Allocation: The distribution of taxable profits is based on the locations where actual value is generated, rather than on jurisdictions with lower tax rates.

3. Enhancement of Transparency: Multinational Enterprises (MNEs) are mandated to prepare and submit comprehensive documentation, including the Local File, Master File, and Country-by-Country Report (CbCR).

4. Facilitates Dispute Prevention: It enables the establishment of Advance Pricing Agreements (APAs), whereby tax authorities and taxpayers concur in advance on transfer pricing methodologies. Aids in the reduction of the frequency of audits and legal disputes.

5. Discourages Tax Avoidance: Reduces the use of artificial pricing arrangements to avoid tax.

Limitations of Transfer Pricing

1. High Compliance Costs: The preparation of Local Files, Master Files, and Country-by-Country Reports (CbCR) involves considerable time, expertise, and financial resources. These present a significant burden, particularly for small and medium-sized enterprises and local subsidiaries of multinational enterprises (MNEs).

2. Risk of Double Taxation: When two nations encounter a discrepancy regarding the appropriate transfer price, there is a potential for the same income to be subject to double taxation.

3. Administrative Burden: The necessity for continuous updates, annual filings, and extensive documentation imposes a significant administrative workload on organisations. This obligation often diverts essential resources from the core business.

Conclusion

The transfer pricing regime is a crucial component of modern tax administration, particularly in economies like Nigeria, which are becoming increasingly integrated into global trade. By ensuring that related-party transactions reflect market-based pricing, the regime supports fair taxation and helps prevent profit shifting. However, the effectiveness of transfer pricing regulations depends heavily on proper enforcement, technical capacity, and the availability of reliable data. To maximise its effectiveness, Nigeria must continue to refine its regulatory framework, invest in technical facilities for the tax authority, promote the use of dispute prevention tools and mechanisms such as, Advance Pricing Agreements (APAs), and strengthen international cooperation. Only then can transfer pricing serve as a balanced tool for both tax fairness and business certainty.

REFERENCES:

• Federal Inland Revenue Service (FIRS)

• Organization for Economic Cooperation and Development (OECD)

Tags

Comments (0)

Leave a Reply

No approved comments yet. Be the first to comment!